Introduction

Alternative Investment Market (‘AIM’) is a sub market of the London Stock Exchange (‘Main Market’) that permits relatively smaller companies to float and list its securities with a more flexible regulatory system than is applicable to Main Market including no set requirements for capitalization or the number of securities issued. AIM is the London Stock Exchange’s global market offering for smaller and growing companies. AIM was conceptualized with the intention to create a more flexible regulatory environment tailored specifically for smaller companies.

AIM was developed to meet the needs of smaller growing companies from any sector or country which might find difficult to meet the full criteria for a listing on the Main Market of the London Stock Exchange or in the respective country. Companies that seek to have their shares traded on AIM range from young and venture capital backed businesses to more established companies looking to expand. In recent years, listing on AIM has been popular with fast growing technology companies.

A key difference between AIM and other markets is that AIM companies are supervised by a nominated adviser (‘Nomad’) rather than by a securities regulator e.g. Financial Services Authority (‘FSA’) in UK. The main body of rules that govern the admission process and on-going obligations of AIM companies are set out in the AIM Rules for companies . AIM’s simplified admission procedure generally results in savings in time and cost for an AIM admission as compared to a Main Market or other listing.

Key Benefits of an AIM offering

1. Access to investors beyond FIIs;

2. High quality but reasonable disclosure, appropriate for smaller companies;

3. World-class profile and branding of London Stock Exchange;

4. Internationalized and diverse capital structure with wider options for future financing;

5. Local financing and investor base in global markets which is globally respected;

6. Offers access to differentiated investor base;

7. Targeted by high growth companies which may not attract investor interest in the main market;

8. Simple regulatory regime providing access to a large pool of diverse, high quality investors;

9. Heightened interest and positioning of the company;

10. Specifically tailored for smaller and younger companies seeking growth capital and providing liquidity to them;

11. Easier reporting & disclosure rules and less stringent requirements in terms of shareholder’s approvals, minimum capitalisation, shareholding requirements and no prior trading record requirements; and

12. Tax benefits for both individual and corporate investors.

Eligibility for admission to trading on AIM

AIM’s admission requirements permit young and growing companies from around the world with limited or no trading records to join the market. The Exchange does not impose any minimum requirements for market capitalisation, trading record, share price or shares in public hands (‘free float’), and the Exchange does not make the decision as to whether a company is suitable for admission to AIM – this responsibility is placed on the Nomad.

Indian Companies listed on AIM

As AIM is one of the world’s leading markets for small, growing, owner-managed and entrepreneurial businesses/growth companies, it suits the profile of Indian businesses as India is an emerging market and also it provides access to foreign capital along-with a qualified investor base. The details of Indian companies listed on AIM are compiled under the section “Case Studies” forming part of chapter 9.

The leading industry sectors for Indian AIM listed companies by market capitalisation are:

a) Energy, exploration and production;

b) Business support services;

c) Infrastructure, real estate holding & development.

Cost of AIM listing

The cost of an AIM listing varies on various factors and can broadly be categorized into 3 baskets:

1. Fees to the AIM exchange:

a. Initial Admission Fees – Based on Market Capitalisation.

b. Admission fees for issuing further securities – For further issues of £5 million and above a fee will apply based on the value of the securities admitted. Charges will only apply to further capital raisings. No further issue fee will apply for further issues where capital raised is below £5 million.

c. Annual Fees – A fixed recurring annual fee (£ 5899 w.e.f. 1st April, 2013) is charged for AIM continuous listing.

2. Brokerage and Marketing costs: The company would need to pay the broker’s fees for raising funds which may range anywhere between 3% and 6% of the funds raised.

3. Advisors and compliance costs: Generally, fees for advisory and support services (including the Nomad’s fees, solicitors’ fees and public relations advisers’ fees) for a straight forward AIM IPO would normally be in the range of £300,000 – £600,000. Fees payable to attorneys and auditors would further add up.

AIM is not a “regulated market”, and unlike the Main Market, there are limited restric¬tions on the ability of an applicant to seek to have its shares admitted to trading on AIM. There is no require¬ment that a minimum number of the shares of the company should be in public hands, and there are no minimum market capitalization norms also. A more principle-based overriding requirement for a company seeking admission to AIM is that it be “appropriate” for the market. This judgment is made by the company’s nominated adviser.

There are also some specific conditions that need to be satisfied in order to facilitate the admission of an issuer to trading on AIM:

General Requirements:

a) Appointment of a Nominated Adviser and Broker

An AIM company must appoint and retain a nominated adviser and broker at all times. In February 2007, the London Stock Exchange introduced AIM Rules for Nominated Advisers with which all nominated advisers must comply.

b) Public Company

Whilst there is no specific requirement under the AIM Rules for an applicant to be a public company, an English company would still need “public company” status in order to enable it to offer shares to the public. For companies incorporated outside UK (including India), the company’s shares need to be capable of being traded under the laws of the country where the AIM company is incorporated.

c) Lock-Ins for New Businesses

Where the issuer’s main activity is a business that has not been independent and earning revenue for at least two years, the AIM Rules require all directors and senior employees of the company to enter into lock-in agreements such that they will not dispose of shares in the company for a period of at least one year following admission, save in limited circumstances.

d) Transferability of Shares

All AIM companies must ensure that their shares are freely transferable except where any jurisdiction, statute or regulation places restrictions upon transferability or where the AIM company is seeking to limit the number of shareholders domiciled in a particular country to ensure that it does not become subject to other statute or regulation.

e) Settlement

Except where the London Stock Exchange otherwise agrees, AIM securities must be eligible for electronic settlement. In practice, the London Stock Exchange has been willing to waive the requirement for securities to be eligible for electronic settlement where this is prohibited by applicable law or regulation.

f) Special Conditions

The London Stock Exchange has a residual ability to require compliance with special conditions as a pre-requisite to admission, although in practice this power is rarely used.

Company specific requirements:

In order to have greater supervision on certain class of companies which are subject to higher risks due to nature of their business activities, the London Stock Exchange has prescribed certain additional eligibility norms in order to secure the interest of investors which are as below:

a) Investing Companies

The definition of investing company does not include an AIM company which is a holding company or as referred as a “topco’” for a trading business, but it does include entities such as cash shells, blank cheque companies and special purpose acquisition companies.

The revised AIM Rules (which incorporate the ‘AIM Note for Investing Compa¬nies’), which became effective on June 1, 2009, provide that:

• Where the applicant is an investing company, a condition of its admission is that it raises a minimum of £3 million in cash via an equity fund raising on, or immediately before, admission.

• An investing company must state and follow an investing policy.

• An investing company must seek the prior consent of its shareholders in a general meeting for any material change to its investing policy.

• Where an investing company has not substantially implemented its investing policy within eighteen months of admission, it should seek the consent of its shareholders for its investing policy at its next annual general meeting and on an annual basis thereafter, until such time that its investing policy has been substantially implemented.

The AIM exchange should be consulted if there is any doubt concerning whether or not an applicant or an existing AIM company should be treated as an investing company.

The AIM Note for Investing Companies clarifies the types of investing companies that the London Stock Exchange considers appropriate for admission to AIM. Broadly, investing companies seeking admission should have straight forward structures, securities and investing policies. Typically, the London Stock Exchange would expect an investing company to be a closed-ended entity of a nature similar to that of a UK public limited company, thus not requiring a restricted investor base. In addition, the Exchange has introduced provisions regarding the need for independence between the board, the nominated adviser and any investment manager, to ensure that both the investment manager and the board are appropriate for AIM and have sufficient experience.

Furthermore, an investment manager and its key employees who are responsible for making investment decisions in relation to the investing company will be considered directors for the purposes of AIM Rules 7 (lock-ins), 13 (related-party transactions), 21 (restrictions on deals) and 17 (disclosure of deals).

There are also new specific disclosure requirements for investment managers of externally managed investing companies that both reflect the key role that managers perform and also recognize that the managers are currently not directly covered by the AIM Rules.

b) Resource Companies

Companies operating in the mining and oil & gas sectors which are admitted or are seeking admission to AIM are referred to as Resource Companies. In response to a growing perception in the market that some Resource Companies being admitted to trading on AIM were too speculative, in March 2006, the London Stock Exchange issued guidance setting out its minimum expectations for Resource Companies. This guidance includes recommendations that, for each admission of a Resource Company, a competent person’s report should be prepared on the assets and liabilities of the company, should be up to date (i.e., no more than six months prior to the date of the admission document) and should be issued by a suitably qualified person. It also recommends that nominated advisers should conduct full due diligence on the company and its assets prior to admission, including undertaking site visits and, where the assets are outside the UK, obtaining legal opinions as to the title to and ownership of the relevant assets. The London Stock Exchange has confirmed that this guidance note forms part of the AIM Rules.

A. THE NOMINATED ADVISER

Each issuer must appoint, and retain, a nominated adviser (often referred to as a “Nomad”) at all times. The London Stock Exchange approves, and maintains a list of corporate finance firms that are qualified to act as Nomads in relation to an AIM issuer. In March 2007, the London Stock Exchange issued a new rule book for nominated advisers (the “Nomad Rules”2), which sets out the eligibility criteria for becoming a Nomad and Nomads’ re-sponsibilities. Ultimately, the judgment and the responsibility as to whether or not a company is appropriate to be admitted to AIM rest with the Nomad and not with the London Stock Exchange.

In addition to assessing the appropriateness of applicants for AIM, a Nomad is also obliged to comply with the Nomad Rules , the AIM Rules, any notices issued by the London Stock Exchange and to act with due skill and care at all times. It must be available to advise and guide the AIM company at all times and must allocate at least two appropriately qualified staff to be responsible for each AIM issuer for which it acts. The Nomad Rules comprise certain “principles” that must be satisfied in all cases and, in respect of each principle, a non-exhaustive list of actions that the London Stock Exchange would normally expect a Nomad to undertake in satisfying that principle.

Nomads’ responsibilities, which are owed principally to the London Stock Exchange, broadly fall into three main categories: a) those that arise in the context of an issuer’s admission to AIM (“Admission Responsibilities”), b) those that apply following the IPO (“Ongoing Responsibilities”) and c) those that arise upon a Nomad’s engagement as Nomad to an existing AIM company (“Engagement Responsibilities”).

Admission Responsibilities (AR)

There are five principles with which a nomad must comply in meeting its AR responsibilities in respect of an issuer’s admission to AIM:

a) “AR1 in assessing the appropriateness of an applicant and its securities for AIM, a nomad should achieve a sound understanding of the applicant and its business.”

Although it is not specifically required under AR1, the London Stock Exchange has said that it expects a nomad to provide advice to the company on the appointment of advisers.

b) “AR2 In assessing the appropriateness of an applicant and its securities for AIM, a nomad should (i) investigate and consider the suitability of each director and proposed director of the applicant; and (ii) consider the efficacy of the board as a whole for the company’s needs, in each case having in mind that the company will be admitted to trading on a UK public market.”

c) “AR3 The nomad should oversee the due diligence process, satisfying itself that it is appropriate to the applicant and transaction and that any material issues arising from it are dealt with or otherwise do not affect the appropriateness of the applicant for AIM.”

d) “AR4 The nomad should oversee and be actively involved in the preparation of the admission document, satisfying itself (in order to be able to give the nomad’s declaration) that it has been prepared in compliance with the AIM Rules for Companies with due verification having been undertaken.”

e) “AR5 the nomad should satisfy itself that the applicant has in place sufficient systems, procedures and controls in order to comply with the AIM Rules and should satisfy itself that the applicant understands its obligations under the AIM Rules.”

The London Stock Exchange also prescribes that the Nomad should be satisfied that there are appropriate procedures in place within the company to enable the relevant people within the company to have a clear understanding of the circumstances in which it should seek the advice of its Nomad.

Nomad Declaration

In addition to complying with the principles described above, the Nomad must also give a declaration to the London Stock Exchange (known as a “Nomad declaration”) confirming that:

• to the best of its knowledge and belief, having made due and careful enquiry and considered all relevant matters under the AIM Rules:

– the admission document complies with Schedule 2 of the AIM Rules; or

– where the applicant is a quoted applicant, the requirements of Schedule 1 (and its supplement) to the AIM Rules have been complied with;

• it is satisfied that the applicant company and its shares are appropriate to be admitted to AIM, having made due and careful enquiry and considered all relevant matters set out in the AIM Rules and the Nomad Rules;

• the directors of the AIM company have received advice and guidance (from its Nomad and other professional advisers) as to the issuer’s responsibilities and obligations under the AIM Rules in order to facilitate due compliance by the company on an ongoing basis; and

• it will comply with the AIM Rules and Nomad Rules applicable to it in its role as Nomad.

The Nomad will typically receive comfort letters from the issuer and its advisers in order to support its declaration.

B. THE ADMISSION DOCUMENT

The admission document or a prospectus is required in two circumstances:

i. where an issuer is making an offer of transferable securities to the public; and

ii. where an issuer is seeking admission to a regulated market.

The rules introduced by the Prospectus Directive in July 2005 and, in particular, the requirement for all prospectuses to be approved by the FSA were viewed by AIM as potentially undermining one of its key competitive advantages: the ability for issuers and their advisers to control their own documents and, consequently, their own fund raising timetables. As a way of partially mitigating these concerns, in October 2004 AIM ceased to be a “regulated market”, becoming an “exchange-regulated market” instead.

As a result of the “de-regulation” of AIM’s status, an AIM IPO or offering will require an FSA-approved prospectus only where an “offer to the public” is also being made. An AIM IPO conducted via an institutional placing will not normally incorporate an “offer to the public” for these purposes and, under the AIM Rules (AR 3), would typically require the publication of an “AIM admission document” instead. The minimum content requirements for an admission document are drafted by reference to the specific requirements of Annexes I to III of the Prospectus Rules, although certain of the more onerous disclosure requirements have been carved out or left to the nominated adviser’s discretion.

Key items carved out include:

a) Pro-forma financial information where there has been a “gross significant change” from historic financial information;

b) The operating and financial review;

c) Capital resources;

d) Research and development, patents and licenses;

e) Administrative, management, and supervisory bodies and senior management;

f) Remuneration and benefits;

g) Working capital;

h) Capitalisation and indebtedness;

i) Interests of those in the offer;

j) Terms and conditions of the offer;

k) Admission to trading and dealing arrangements; and

l) Documents on display.

AIM companies are required to prepare their financial statements in accordance with the IFRS in respect of financial years commencing on or after January 1, 2007. Under Schedule 2 of the AIM Rules, historic financial information included in admission documents in respect of financial periods prior to that date may be presented in accordance with UK GAAP rather than the IFRS.

Items carved out on Qualified Basis:

As mentioned above, in addition to items carved out altogether, certain items have been carved out on a “qualified basis”, which means that they may be excluded at the discretion of the nominated adviser. These items include:

i. Principal markets; and

ii. Shareholdings and share options of non-board members of senior management.

In addition to the content requirements derived from the Prospectus Rules , the requirements of Schedule 2 to the AIM Rules must also be adhered to. A competent person’s report will also generally be required in the context of a Resource Company seeking admission to AIM.

An issuer must also satisfy a general duty to disclose in an AIM admission document any other information it considers necessary to enable investors to form a full understanding of (i) the assets and liabilities, financial position, profits and losses, prospects of the applicant and its securities; (ii) the rights attaching to those securities; and (iii) any other matter contained in the admission document.

In view of an issuer’s overriding general duty to disclose all material information, and of the responsibility reserved to the nominated advisers in ensuring compliance with the rules, there may well be cases where “carved-out” items ought to be disclosed as a matter of best practice.

C. ANCILLARY DOCUMENTATION

1) 10-Day Announcement

The applicant must provide to the London Stock Exchange, at least 10 business days before the expected date of admission to AIM (known as a “pre-admission announcement”), the information specified by Schedule 1 of the AIM Rules (AR2). This includes:

a) the company’s name, address and country of incorporation;

b) a description of the company’s business;

c) the number and type of securities for which it is seeking admission (and detailing the number and type of securities to be held as treasury shares);

d) an indication of whether it will be raising capital on admission;

e) the names, addresses and functions of the directors and proposed directors;

f) the persons who are interested in 3 percent or more of its securities;

g) its anticipated accounting reference date;

h) the name and address of its nominated adviser and broker; and

i) details of where the admission document will be available

Quoted applicants are required to produce additional information as set out in the supplement to Schedule 1 of the AIM Rules.

2) Other Application Documents

At least three business days before the expected date of admission, an applicant must submit to the London Stock Exchange:

a) An electronic version of its Admission Document;

b) A completed application form; and

c) A declaration in the prescribed form under Schedule 2 of the Nomad Rules from the nominated adviser.

3) AIM Fee

Fees are now payable on the basis of a post-admission invoice, rather than submitted three days before admission.

D. FAST TRACK TO AIM

There is a fast-track admission route to AIM for certain existing quoted companies. The rules permit companies that are already listed on the Australian Securities Exchange, Euronext, the Deutsche Börse, the JSE Securities Exchange South Africa, NASDAQ, the New York Stock Exchange, the Stockholms borsen, the SIX Swiss Exchange, the Toronto Stock Exchange or the UK’s Main Market (referred to as “designated markets”, a current list of which can be found on the London Stock Exchange web site) and that have been trading on a designated market for at least 18 months to use their existing annual reports and accounts as a basis for admission to trading on AIM.

Issuers wishing to use the expedited admission route will need to comply with limited eligibility conditions and will need to appoint a nominated adviser and broker.

The key advantage of the fast-track route is that an issuer’s annual report and accounts take the place of the admission document and are simply supplemented by a fuller pre-admission announcement. Admission on this expedited basis will require the following:

a) At least 20 business days before the expected date of admission, the issuer will need to submit to the London stock Exchange the information required by the “10-day announcement” referred to above, plus:

• the name of the designated market on which it has been traded and the date from which it has been traded on such market;

• confirmation that, following due and careful enquiry, it has adhered to any legal and regulatory requirements involved in having a listing on the relevant desig¬nated market;

• a web site address where the company’s latest published report and accounts, recent public documents and announcements it has made public over the last two years and details of the rights attaching to its securities can be viewed (and where more than nine months have elapsed since the financial year-end to which its most recent annual accounts relate, interim results covering no less than the six months from the year-end will also be required to be available on a web site);

• details of its intended strategy following admission;

• a description of any significant change in the financial or trading position of the issuer that has occurred since the end of the last financial period for which audited accounts have been prepared;

• a statement confirming that the issuer’s directors have no reason to believe that the working capital available to the issuer or its group will be insufficient for at least 12 months from admission;

• details of any lock-in arrangements required pursuant to the AIM Rules;

• a brief description of the arrangements for settling transactions in its securities;

• any other information that has not been made public and that would other¬wise be required to be disclosed in an admission document if the standard route had been followed; and

• the number of each class of securities held as treasury shares.

b) At least three business days before the expected date of admission, the issuer will need to submit to the London stock Exchange:

• an electronic version of its latest report and accounts;

• a formal application for the admission of the securities;

• the nomad’s declaration referred to above; and

• the relevant AIM fee.

Whilst nowhere near as detailed as those applicable to companies listed on the Main Market, the continuing obligations with which an AIM company is required to comply are derived from broadly the same principles as their Main Market counterparts.

A. GENERAL OBLIGATION OF DISCLOSURE

Under AIM Rule 11, an AIM company must notify the Regulatory Information Services (RIS) without delay of any new developments that are not in public knowledge concerning a change in its financial condition, its sphere of activity, the performance of its business or its expectation of own perform¬ance, which, if made public, would likely to be lead to a substantial movement in the price of its AIM securities.

The AIM company must take care that any information it provides is not misleading, false or deceptive and does not omit anything likely to affect the import of such in¬formation, and it must provide the information no later than it is published elsewhere.

B. SPECIFIC DISCLOSURE OBLIGATIONS

a) Miscellaneous information (AR 17)

An issuer must notify a RIS without:

• delay of any deals by directors;

• any changes to the holding of a significant shareholder (3 percent holder) that increases or decreases such holding through a single percentage;

• the resignation, dismissal or appointment of any director;

• any change in its accounting reference date;

• any material change between its actual trading performance or financial condition and any profit forecast, estimate or projection included in its admission document or otherwise made public on its behalf;

• any decision to make any payment in respect of its AIM securities;

• the reason for the application for admission or cancellation of any AIM securities;

• the resignation, dismissal or appointment of its nominated adviser or broker; any change in the AIM company’s legal name or registered office;

• the occurrence and number of shares taken into and out of treasury;

• any change in the web site address at which information required by AIM Rule 26;

• any subsequent change to certain details disclosed in respect of a director; and

• The admission to trading (or cancellation from trading) of the AIM securities (or any other securities issued by the relevant AIM company) or any other exchange or trading platform, where such admission or cancellation is at the application or with the agreement of the AIM company.

b) Half-Yearly Reports

An AIM company must prepare a half-yearly report in respect of the six-month period from the end of the financial period for which financial information has been disclosed in its admission document and at least every subsequent six months thereafter (apart from the final period of six months preceding its accounting reference date for its annual audited accounts). All such reports must be notified to the RIS without delay and in any event not later than three months after the end of the relevant period. The information contained in a half-yearly report must include at least a balance sheet, income statement and cash flow statement and must contain comparative figures for the corresponding period in the preceding financial year. The report must also be presented and prepared in a form consistent with that which will be adopted in the company’s annual accounts, having regard to the applicable accounting standards. The Guidance Notes in the AIM Rules state that when the half-yearly report has been audited, it must contain a statement to this effect.

c) Annual Accounts

An AIM company must publish annual audited accounts that must be sent to the holders of its AIM securities without delay and in any event not later than six months after the end of the financial period to which they relate. An AIM company incorporated in an EEA State must prepare its accounts in accordance with the IFRS. An AIM company incorporated in a non-EEA State may prepare its accounts in accordance with IFRS, US GAAP, Canadian GAAP, Australian IFRS or Japanese GAAP

These accounts must disclose any transaction with a related party, whether or not previously disclosed under the AIM Rules, where any of the class tests , (which are settled out in Schedule Three of the AIM Rules which determine whether certain rules are applicable or not), exceed 0.25 percent and must specify the identity of the related party and the consideration for the transaction.

d) Publication of Documents Sent to Shareholders

Any document provided by an AIM company to its shareholders must be made available on its web site, and this must be publicized. An electronic copy of the relevant document must also be sent to the London Stock Exchange.

e) Company Information Disclosure

An AIM company must, from admission, maintain a web site on which the following information should be made available free of charge:

• a description of its business and, where it is an investing company, its investing policy and details of any investment manager and or key personnel;

• the names of its directors and brief biographical details of each;

• a description of the responsibilities of the members of the board and details of any board committees and their responsibilities;

• its country of incorporation and main country of operation;

• where the AIM company is not incorporated in the UK, a statement that the rights of shareholders may be different from the rights of shareholders in the UK-incorporated company;

• its current constitutional documents;

• details of any other exchanges or trading platforms on which it has applied or agreed to have any of its securities admitted or traded;

• the number of AIM securities in issue and, insofar as it is aware, the percentage of AIM securities that are not in public hands, together with the identity and percentage holdings of its significant shareholders;

• details of any restrictions on the transfer of its AIM securities;

• its most recent annual report and all half-yearly, quarterly or similar reports published since the last annual report;

• its most recent admission document, together with any circulars or similar pub-lications sent to shareholders within the past 12 months; and

• details of its nominated adviser and other key advisers.

Nomad’s Responsibility:

a) Ongoing Responsibilities (OR)

Nomads must satisfy the following principles on a continuing basis:

“OR1 The Nomad should maintain regular contact with an AIM company for which it acts, in particular so that it can assess whether (i) the Nomad is being kept up to date with developments at the AIM company; and (ii) the AIM company con¬tinues to understand its obligations under the AIM Rules.”

“OR2 The Nomad should undertake a prior review of relevant notifications made by an AIM company with a view to ensuring compliance with the AIM Rules.”

“OR3 The Nomad should monitor (or have in place procedures with third parties for monitoring) the trading activity in securities of an AIM company for which it acts, especially when there is unpublished price-sensitive information in rela¬tion to the AIM company.”

“OR4 The Nomad should advise the AIM company on any changes to the board of directors the AIM company proposes to make, including (i) investigating and considering the suitability of proposed new directors; and (ii) considering the effect any changes could have on the efficacy of the board as a whole for the company’s needs, in each case having in mind that the company is admitted to trading on a UK public market.”

b) Engagement Responsibilities (ER)

When a Nomad is being appointed by an existing AIM company, it must comply with the following:

“ER1 In assessing the appropriateness of an AIM company and its securities for AIM when taking on an existing AIM company, a Nomad should achieve a sound understanding of the AIM company and its business.”

“ER2 In assessing the appropriateness of an existing AIM company and its securities for AIM, a Nomad should (i) investigate and consider the suitability of each di¬rector and proposed director of the AIM company; and (ii) consider the efficacy of the board as a whole for the company’s needs, in each case having in mind that the company is admitted to trading on a UK public market.”

“ER3 The Nomad should satisfy itself that the AIM company has in place sufficient systems, procedures and controls in order to comply with the AIM Rules and should satisfy itself that the AIM company and its directors understand their obligations under the AIM Rules.”

C. RESTRICTIONS ON DEALS

Under AR 21, an AIM company must ensure that its directors and “applicable em¬ployees” (who, for these purposes, are defined as employees who are likely to be in possession of unpublished price-sensitive information) do not deal in any of its AIM securities during the period of two months preceding the publication of annual results and half-yearly reports and, if it reports on a quarterly basis, one month prior to the notification of its quarterly results. This rule also restricts the sale or redemption of securities held as treasury shares during such a period.

D. CORPORATE TRANSACTIONS

a) Substantial Transactions (AR 12)

An AIM company must notify a RIS without delay as soon as the terms of any sub-stantial transaction are agreed. A “substantial transaction” is one that exceeds 10 percent in any of the class tests specified in Schedule 3 to the AIM Rules, save for any transactions of a revenue nature in the ordinary course of business and transactions to raise finance that do not involve a change in the fixed assets of the AIM company or its subsidiaries. As is the case on the Main Market, each class test involves a comparison between the size of the transaction (or the target of the transaction (as applicable)) and the AIM company.

b) Related-Party Transactions (AR 13)

This rule applies to any transaction whatsoever with a related party that exceeds 5 percent in any of the class tests specified under “Substantial Transactions” above.

An AIM company must notify a RIS without delay as soon as the terms of a transaction with a related party are agreed. The announcement is required to include the details specified by Schedule 4 to the AIM Rules and a statement that with the exception of any director who is involved in the transaction as a related party, its directors, having consulted with its nominated adviser, consider that the terms of the transaction are fair and reasonable insofar as the holders of its AIM securities are concerned.

c) Reverse Takeovers (AR 14)

A “reverse takeover” is an acquisition or acquisitions in a 12-month period that for an AIM company would:

• exceed 100 percent in any of the class tests;

• result in a fundamental change in its business, board or voting control; or

• in the case of an investing company, depart materially from its investing policy as stated in its admission document or approved by shareholders in accordance with the AIM Rules.

Any agreement that would effect a reverse takeover must be:

• conditional on the consent of the holders of its AIM securities being given in general meeting;

• notified to a RIS without delay, disclosing the information specified in Schedule 4 of the AIM Rules and, insofar as it is with a related party, the additional information stated above under “Related-Party Transactions”; and

• accompanied by the publication of an admission document in respect of the proposed enlarged entity and convening the general meeting.

Where a shareholder approval is given for the reverse takeover, trading in the AIM securities of the AIM company will be cancelled. If the enlarged entity seeks admission, it must make an application in the same manner as any other applicant applying for admission of its securities for the first time.

d) Disposals Resulting in a Fundamental Change of Business (AR 15)

Any disposal by an AIM company that, when aggregated with any other disposal or disposals over the previous 12 months, exceeds 75 percent in any of the class tests is deemed to be a disposal resulting in a fundamental change of business and must be:

• conditional on the consent of its shareholders being given in general meeting;

• notified to a RIS without delay, disclosing the information specified by Schedule 4 of the AIM Rules and, insofar as it is with a related party, the additional information stated under “Related-Party Transactions” above; and

• accompanied by the publication of a circular containing the information specified above and convening the general meeting.

Where the effect of the proposed disposal is to divest the AIM company of all, or substantially all, of its trading business activities, the AIM company will, upon disposal, be treated as an investing company from the date the shareholder consent is given under AR 15, and the notification and circular containing the information specified by Schedule 4 to the AIM Rules convening the general meeting must also state its investing policy going forward, which must also be approved by shareholders.

The AIM company will then have to make an acquisition or acquisitions that constitute a reverse takeover under AR 14 or otherwise implement the investing policy approved at the general meeting to the satisfaction of the London Stock Exchange within 12 months of becoming an investing company.

e) Aggregation of Transactions

Transactions completed during the prior 12 months must be aggregated for the purposes of determining whether AIM Rule 12, 13, 14 or 15 applies where they are entered into by the AIM company with the same person or persons or their families or where they involve the acquisition or disposal of securities or an interest in one particular business, or where together they lead to a principal involvement in any business activity that did not previously form a part of the AIM company’s principal activities.

E. CONTENTS OF ANNOUNCEMENT (SCHEDULE 4)

The details that must be announced pursuant to AIM Rules 12, 13, 14 and 15 in the event of any of the transactions referred to above are as follows:

• particulars of the transaction, including the names of any other parties, where relevant;

• a description of the assets that are the subject of the transaction or the business carried on by, or using, the assets that are the subject of the transaction;

• the profits attributable to those assets, if different from the consideration; the value of those assets;

• the full consideration and how it is being satisfied;

• the effect on the AIM company;

• details of the service contracts of any proposed directors;

• in the case of a disposal, the application of any sale proceeds;

• in the case of a disposal, if shares or other securities are to form part of the consideration received, a statement whether such securities are to be sold or retained; and

• any other information necessary to enable investors to evaluate the effect of the transaction upon the AIM company.

F. BREACH AND ENFORCEMENT

a) Companies

Pursuant to the procedures set out in the Disciplinary Procedures and Appeals Handbook if the London Stock Exchange considers that a company has contra¬vened the AIM Rules, it may take one or more of the following measures (AR 42):

• issue the company a warning notice;

• fine or censure such company;

• publish the fact that the company has been fined or censured and the reasons for that action; or

• cancel the admission of the company’s AIM securities.

b) Nomads

Pursuant to the procedures set out in the Disciplinary Procedures and Appeals Handbook, if the London Stock Exchange considers that a nomad is either in breach of its responsibilities under the AIM Rules or the Nomad Rules or that the integrity and reputation of AIM has been or may be impaired as a result of the nomad’s conduct or judgment, it may take one or more of the following actions:

• issue a warning notice;

• fine or censure such nomad;

• remove the nomad from the register; or

• publish the action it has taken and the reasons for that action.

c) Recent Enforcement

The London Stock Exchange actively monitors compliance with the AIM Rules for

Companies and the AIM Rules for Nominated Advisers and takes action where companies or nomads breach those rules. The London Stock Exchange canissue both public and private censures, though the former are reserved for the most serious cases, generally involving significant market impact.

Renewed focus has been placed on rules relating to the timing and accuracy of disclosures and proper consultation with nomads. In particular, the London Stock Exchange has repeatedly drawn attention to breaches of AR 10 (Principles of Disclosure), AR 11 (General Disclosure of Price Sensitive Information) and AR 31 (Responsibility for Compliance).

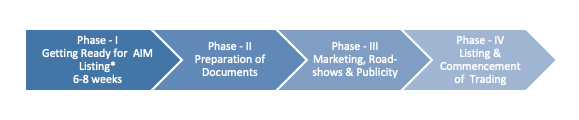

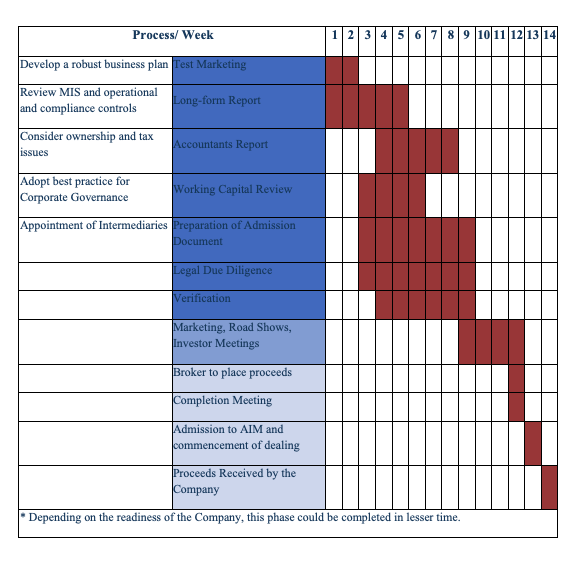

Process & Indicative Time Lines

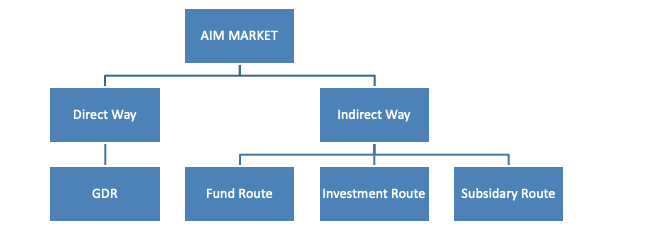

SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009 allows only listed Indian Companies to be listed on other exchanges outside India. An Indian unlisted company cannot list its securities in markets abroad without being listed in India or agreeing to get listed in India within a time-frame.

Direct Way

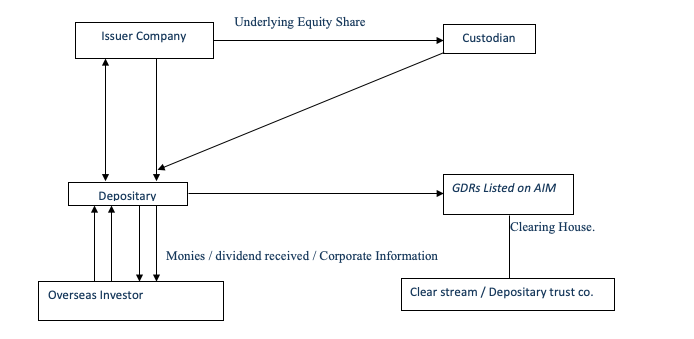

• GDR Route for Listed Entities

• Fund Structure Route

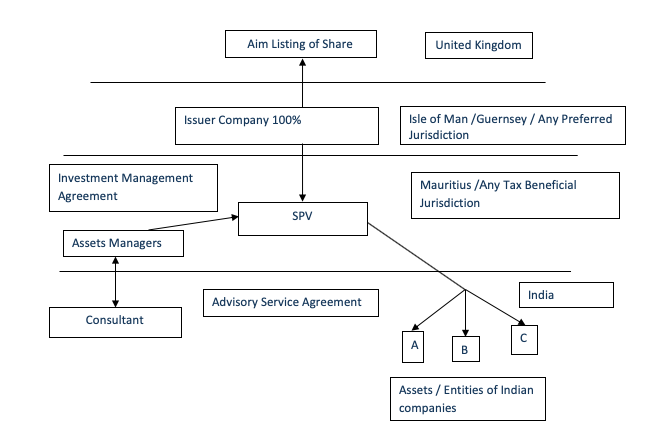

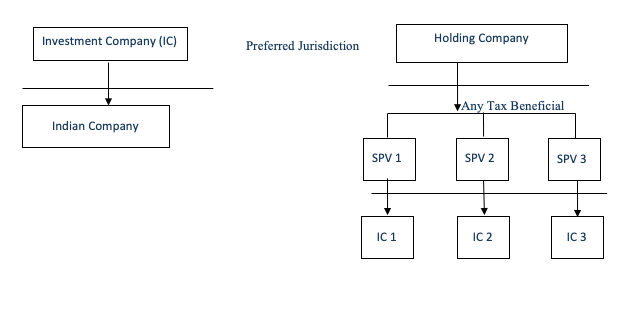

The Company A which is going to be listed on AIM should be a public company limited by shares. The Company A will acquire interests in the eligible Projects located in India. The Company A intends to make investments in Company B (Holding company /Investment company) which may be incorporated in any preferred jurisdiction country which will in turn invest through its Subsidiaries / Project Company / Special Purpose Vehicle’s (SPV) and same will in turn invest into Indian Projects.

• Investment / Holding Company Route

As at 30th April, 2013, there are 21 entities, which are part of corporate houses having business presence in India, traded on AIM with a market capitalisation of approximate £3.70 billion.

;

| Sr. No. | Amount Raised(£m) | AIM rules | Market Cap as on 30/4/2013 (£m) | Percentage increase/(decrease) in market cap since listing (%) |

|---|---|---|---|---|

| 1 | DQ ENTERTAINMENT PLC | 48.91 | 9.00 | (81.60) |

| 2 | EIH PLC | 33.15 | 22.29 | (32.77) |

| 3 | ELEPHANT CAPITAL PLC | 50.00 | 15.30 | (69.41) |

| 4 | EREDENE CAPITAL | 118.29 | 46.15 | (60.98) |

| 5 | EROS INTERNATIONAL PLC | 176.00 | 298.36 | 69.52 |

| 6 | GREENKO GROUP PLC | 66.40 | 192.09 | 189.30 |

| 7 | HIRCO PLC | 382.63 | 29.66 | (92.25) |

| 8 | IENERGIZER LTD | 174.01 | 554.66 | 218.75 |

| 9 | INDIA CAPITAL GROWTH FUND | 75.00 | 28.41 | (62.12) |

| 10 | INDUS GAS LTD | 299.98 | 1,655.91 | 452.01 |

| 11 | INFRASTRUCTURE INDIA PLC | 159.63 | 95.52 | (40.17) |

| 12 | ISHAAN REAL ESTATE PLC | 180.00 | 68.65 | (61.86) |

| 13 | JUBILANT ENERGY N.V. | 320.56 | 60.36 | (81.17) |

| 14 | MORTICE LTD | 31.01 | 28.38 | (8.46) |

| 15 | MYTRAH ENERGY LTD | 188.18 | 164.86 | (12.39) |

| 16 | NOIDA TOLL BRIDGE CO* | 81.87 | 28.46 | (65.24) |

| 17 | OPG POWER VENTURE PLC | 172.19 | 208.27 | 20.95 |

| 18 | PHOTON KATHAAS PRODUCTIONS LTD | 13.84 | 2.64 | (80.92) |

| 19 | SKIL PORTS & LOGISTICS LTD | 110.00 | 51.04 | (53.60) |

| 20 | UNITECH CORPORATE PARKS PLC | 360.00 | 133.20 | (63.00) |

| 21 | WEST PIONEER PROPERTIES LTD | 63.49 | 8.20 | (87.09) |

*Exchange Rate is 1(£) =1. 74517 ($) as per www.xe.com as on 21/3/2007

Source:- Website of London Stock Exchange- AIM

Note: The above calculation of percentage increase / decrease in Market Cap is based on comparison of Market Cap as on date of listing and Market cap as on 30/4/2013, hence it reflects both fluctuations due to price and due to change in capital structure during the covered period.

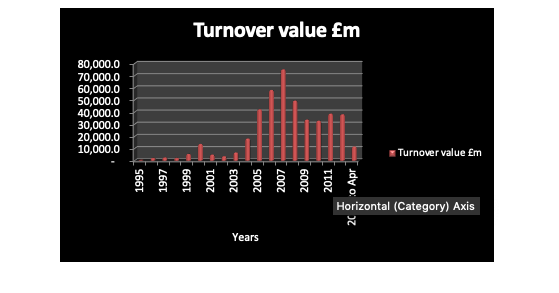

b. Trading turnover since launch:

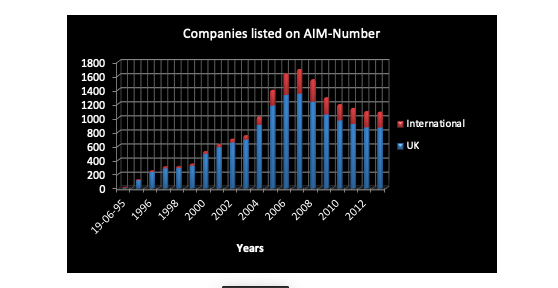

c. No. of Companies listed on AIM since launch:

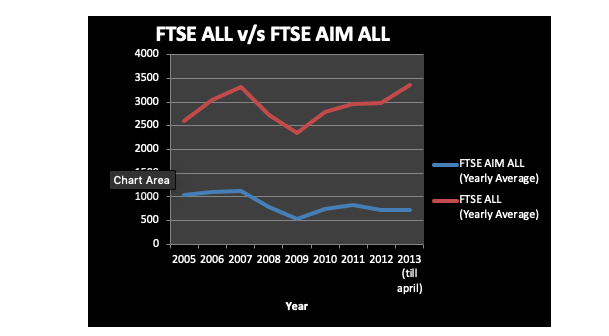

d. Index Performance

The AIM All-Share Index possesses higher variance in comparison to Financial Times Stock Exchange All Industrial Average but not a substantially worse or better performance overall. Even though many small-cap firms traded on the more privately regulated AIM have faced tough times in recent years, as have firms on more regulated markets. Yet AIM has enabled many smaller firms to raise money and has provided more investment outlets to investors.

| Main Market | AIM |

|---|---|

| 1. Minimum public holding requirement | |

| Minimum 25% shares in one or more EEA States* | Not required |

| 2. Trading Record requirement | |

| Three year trading record and audited accounts required | Not required |

| 3. Offering Document to be approved by FSA (or competent authority in issuer’s home member state, where not the UK) requirement | |

| Required | Not required unless IPO is being undertaken in conjunction with an “offer to the public”** |

| 4. Mediator requirement | |

| Sponsor required for IPO and certain transactions | Nominated adviser required at all times |

| 5. Shareholder’s approval requirement for substantial acquisitions and disposals | |

| Prior approval required | No prior shareholder approval required (other than for reverse takeovers) |

| 6. Minimum market capitalisation requirement | |

| £700,000 | Not required |

| 7. Requirement for scientific research based companies and mineral companies | |

| Modifications to the requirement for accounts covering three years | Not required |

* For these purposes, shares held by persons in non-EEA States will be taken into account only if the shares are listed in the non-EEA State in question. Furthermore, shares held by directors, their connected persons, persons with the contractual right to nominate a director, trustees of an employee share scheme and any person (or persons in the same group) with an interest in 5% or more of the shares of the relevant class will not be held “in public hands” for these purposes.

** Scientific research based companies and mineral companies may be eligible for listing even without accounts covering a three-year period, provided certain other conditions are met.

AIM is one of world’s leading market for small, growing, owner-managed and entrepreneurial businesses/ growth companies. It suits the profile of Indian businesses as India is an emerging market and has a large number of entrepreneurial ventures. There is growing interest by Indian companies as it provides access to foreign capital and eligible investors under Indian legal framework. In short, AIM is a market on London stock Exchange enabling small companies to raise capital and have their shares traded in a market without the expenses of a main market listing. AIM is intended to create a more flexible regulatory environment tailored specifically for smaller companies.

The source of this research is inclusive of various publicly available information, data and statistics from various sources including the internet. Reliability of these sources of information and their copyright protections has not been independently verified by us.

Interested in this topic or wanting to know more? Share your thoughts and we will be happy to assist.